.webp)

Let's be honest debt can feel suffocating. One missed EMI, then another, and suddenly your phone is buzzing with bank notices and your CIBIL score is quietly crashing. If you've been in that spot, you already know how scary it feels.

But here's the thing banks don't always want to drag you to court. It's expensive for them too. That's exactly where loan settlement comes in.

So, What Exactly Is Loan Settlement?

Loan settlement (also called debt settlement or one-time settlement) is a process where you and your lender agree to close your loan by paying a reduced lump sum amount less than what you actually owe.

For example if you owe ₹5 lakhs to a bank and you've been defaulting for months, the bank may agree to settle for ₹3 to ₹3.5 lakhs if you can pay it in one shot. They mark the account as "settled" and the loan is closed.

It's not a magic trick. It's a real, legal process that banks and NBFCs accept especially when they feel recovering the full amount is unlikely.

Who Can Go for Loan Settlement in India?

Loan settlement is typically for people who are genuinely struggling not those who can pay but simply don't want to. Banks look at your situation carefully. You may be eligible if:

Typical eligibility signals

- 1You've missed 3 or more EMIs (technically a "NPA" account)

- 2You've lost your job, faced a medical emergency, or a business shutdown

- 3You genuinely can't repay the full outstanding amount

- 4You have some lump sum amount from family, savings, or asset sale

How Does the Loan Settlement Process Work?

The process isn't complicated, but it does require patience and the right approach. Here's how it usually goes:

Step-by-step settlement process

- 1 - Assess your debt - Know exactly how much you owe, including principal, interest, and penalties.

- 2 - Approach the bank - Write to the bank's grievance or recovery team expressing your intent to settle.

- 3 - Make a settlement offer - Typically 40–70% of the outstanding amount, depending on your case.

- 4 - Negotiate Banks may counter-offer. This is where having a professional helper makes a big difference.

- 5 - Get the agreement in writing A- lways get the settlement letter before making any payment.

- 6Pay and close - Pay the agreed amount, collect your NOC (No Objection Certificate) and closure documents.

The Honest Truth Pros and Cons

Loan settlement has real benefits, but it's not without trade-offs. Here's a clear picture:

Benefits

- Pay less than you owe

- Stop recovery agent harassment

- Legally close the loan

- Avoid court proceedings

- Start fresh financially

Watch out for

- CIBIL score drops significantly

- Account marked "Settled" (not "Closed")

- May affect future loan eligibility

- Need lump sum ready upfront

- Negotiation can take time

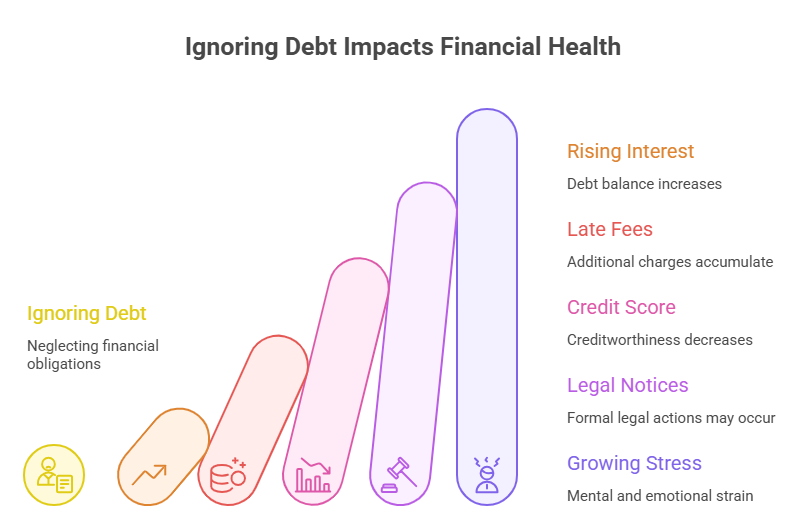

What Happens to Your CIBIL Score After Settlement?

This is the part most people worry about and they should know the truth. When your loan is settled, your credit report shows the account status as "Settled" instead of "Closed". This tells future lenders that you didn't pay the full amount.

Your CIBIL score will drop sometimes significantly. But here's the reassuring part: this is not permanent. With responsible financial behaviour paying bills on time, using credit wisely your score can recover over 2–4 years. Many people have bounced back successfully after settlement.

Can You Do Loan Settlement on Your Own?

Technically, yes you can approach the bank yourself. But in reality, negotiating with a bank without experience is tough. Banks have trained recovery teams; you're often talking to people who negotiate daily. Most people end up paying more than they should, or the process drags on for months.

That's why many people in India now use professional loan settlement services companies that know exactly how to negotiate, what to say, and how to get you the best possible deal.

Types of Loans That Can Be Settled in India

Loans typically eligible for settlement

- Personal loans from banks and NBFCs

- Credit card outstanding dues

- Business loans (MSME / SME)

- Home loans (in some NPA cases)

- Gold loans, vehicle loans, education loans

The Bottom Line

Loan settlement in India is a genuine lifeline for people who are stuck in debt with no clear way out. It lets you pay a reduced amount, legally close your loan, and stop the harassment so you can finally breathe again and start rebuilding.

It's not a perfect solution, and it does come with a temporary hit to your credit score. But for many people, it's the most practical and humane way to get a second chance.

If you're considering this path, get proper guidance. Don't negotiate blindly and don't pay anyone without a written settlement letter in hand.