.jpg)

You swiped. You paid the minimum. You swiped again.And now the bill you thought was ₹50,000 somehow reads ₹90,000 and it is still climbing.

And now the bill you thought was ₹50,000 somehow reads ₹90,000 and it is still climbing.

That is not bad luck. That is how credit card interest works in India. Most cards charge 40–50% annually on outstanding balances. Pay just the minimum every month and you are barely touching the principal. The bank keeps winning. You keep losing.

If this sounds familiar, credit card settlement might be your exit. Here is everything you need to know without the jargon.

What Is Credit Card Settlement?

Credit card settlement is when you negotiate with your bank to close your outstanding dues for less than the full amount or convert that debt into something far more manageable.

It is not a scam. It is not a last resort for people who "failed" financially. It is a structured, legal process that banks themselves participate in because recovering something is better than recovering nothing.

Settlement is typically considered when:

- Your outstanding balance keeps growing despite monthly payments

- Interest charges are piling faster than you can pay them down

- You are trapped paying only the minimum due month after month

- You cannot realistically pay the full amount in the near future

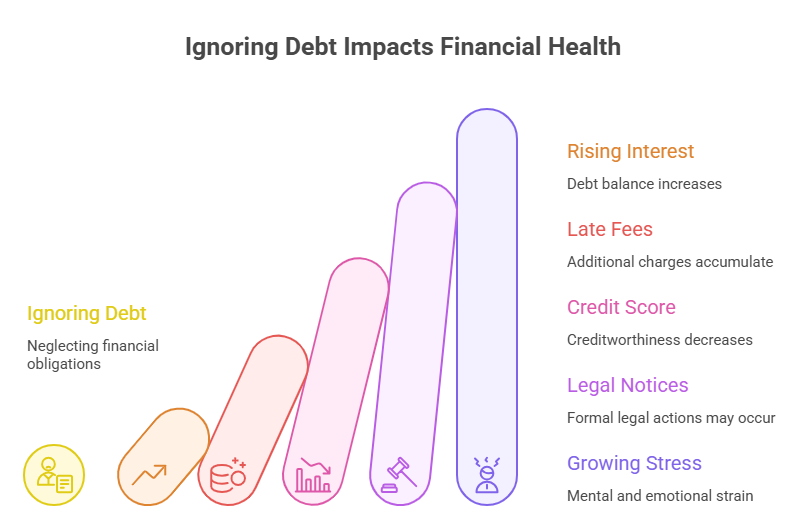

Why Credit Card Debt Spirals So Fast

Here is the math most people do not see coming.

Say your outstanding balance is ₹1,00,000.

At 42% annual interest, you are paying roughly ₹3,500 every single month just in interest before touching the principal. If you pay ₹4,000 as your minimum due, only ₹500 goes toward actually reducing what you owe.

At that rate, clearing ₹1 lakh takes years and costs you significantly more than that in total interest paid.

This is not a budgeting problem. It is a structural trap. And the only way out is to either clear it aggressively or settle it smartly.

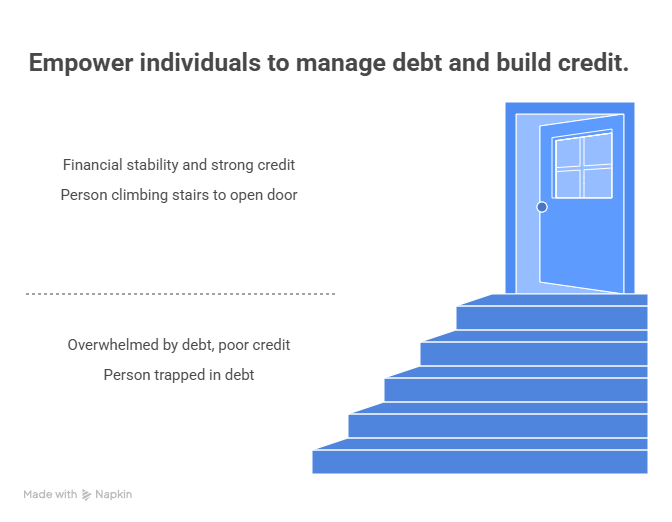

How Credit Card Settlement Actually Works

There are two main paths:

Path 1 Traditional Settlement

You negotiate directly with your bank to accept a lump sum that is less than the total outstanding. The bank agrees, you pay, the account is marked as "settled" and closed.

The downside: your credit score takes a hit because "settled" signals you did not repay in full. But if you are already missing payments, your score is already suffering. Settlement stops the damage and gives you a clean exit.

Path 2 Debt Conversion (The Smarter Route)

Instead of settling at a discount, you replace your high-interest credit card debt with a lower-interest personal loan.

- Credit card interest: 40–50% annually

- Personal loan interest: ~10% annually

Same debt. One-fifth the cost. Fixed EMIs. No more compounding nightmare.

This is the approach Zavo uses and it is far kinder to your credit score.

The Step-by-Step Process

Step 1 - Know your total outstanding Add up the principal, interest, and penalties. You need the real number, not the "minimum due."

Step 2 - Assess if you can pay in full If yes, pay it and move on. If no, settlement is your next move.

Step 3 - Choose your settlement approach Traditional negotiation or debt conversion depending on your financial position and credit score priorities.

Step 4 - Negotiate with the lender This is where most people struggle alone. Banks have internal policies on what they will and will not accept. Knowing the right department, the right offer amount, and the right timing matters enormously.

Step 5 - Get everything in writing A verbal agreement means nothing. Insist on a settlement letter and a No Objection Certificate (NOC) once payment is made. This is the document that protects you legally.

Does Credit Card Settlement Hurt Your CIBIL Score?

Yes if done the traditional way (where the account is marked "settled" rather than "closed"). It signals to future lenders that you did not repay the full amount.

But here is the context that matters:

If you are already missing payments, your CIBIL score is already falling. Every missed EMI, every 90-day default marker these hurt more, for longer. A settlement stops the bleeding and gives you a defined point from which to rebuild.

With consistent credit behaviour after settlement paying new dues on time, keeping utilisation low most people see meaningful score recovery within 12 to 24 months.

The debt conversion route (settling via a personal loan) is even better for your score. You clear the full credit card outstanding, no "settled" mark appears, and you rebuild credit while repaying the personal loan cleanly.

Why Zavo Makes This Easier

Zavo is India's most trusted debt settlement platform — built specifically for people stuck in exactly this situation.

Here is what makes Zavo different:

They do not just settle they convert. Zavo's primary approach is replacing your high-interest credit card debt with a lower-interest personal loan. This means lower monthly outgo, no compounding interest, and no "settled" mark on your credit report.

97% success rate. Not a marketing number. A track record built across thousands of real credit card and loan settlements with Indian banks and NBFCs.

No middlemen. Zavo negotiates directly with your lender. No agents, no referral chains, no unnecessary costs passed to you.

Cashback on settlement. Once your credit card debt is resolved through Zavo, you receive cashback. No other platform in India does this.

Full transparency. Every step of your case is visible inside the Zavo app — what was offered, what was agreed, what documents you will receive. No chasing. No surprises.

The Bottom Line

Credit card debt at 40–50% annual interest is not a problem you can wait out. Every month of inaction costs real money and moves the total further from your reach.

Credit card settlement whether through traditional negotiation or the smarter debt conversion route gives you a structured, legal path to close the liability and start over.

The key is acting before the debt gets bigger. And doing it with someone who knows how.

CTA: Struggling with credit card dues? Let Zavo handle the negotiation Download the Zavo app and take the first step today.

5 FAQs

Q1. What is credit card settlement in simple terms?

It is when you and your bank agree to close your outstanding credit card balance either at a reduced amount or by converting it into a more manageable loan.

Q2. Is credit card settlement legal in India?

Yes. It is a fully legal process. Banks participate in it because recovering partial payment is better than recovering nothing from a defaulting borrower.

Q3. Will settling my credit card destroy my credit score?

Traditional settlement marks the account as "settled," which impacts your score. But if you are already missing payments, your score is already falling. Settlement stops the damage. The debt conversion route (via personal loan) has a much smaller impact on your score.

Q4. How much of my credit card debt can I settle for?

It depends on your lender, the total outstanding, and how long you have been in default. A settlement expert can negotiate the best realistic terms for your specific situation.

Q5. How does Zavo help with credit card settlement?

Zavo replaces your high-interest credit card dues with a lower-interest personal loan clearing your bill immediately and letting you repay in fixed, predictable EMIs at a fraction of the original interest rate.