.webp)

Trying to settle a personal loan in India but not sure where to start? This guide covers exactly what it means, when it makes sense, how the step-by-step process works, and why thousands of Indians are using Zavo to get it done faster and for less.

Personal loans are easy to take and hard to escape when things go wrong. A job loss. A medical bill that wiped out savings. A salary cut that made three EMIs feel impossible. If any of that sounds familiar, settling your personal loan might be the most practical and legal path forward and this guide explains the whole thing in plain, simple words.

What Does It Mean to Settle a Personal Loan?

When you settle a personal loan, you negotiate with your bank or NBFC to close the outstanding account by paying a reduced lump-sum amount less than the total you owe including interest and penalties. The lender accepts this payment as full and final closure and marks the loan as settled.

This process is called a One-Time Settlement or OTS. It is completely legal and is permitted under RBI guidelines. Banks prefer recovering something rather than spending years chasing someone who genuinely cannot repay that is the logic that makes settlement work.

Most borrowers in India who settle a personal loan close the account for 40 to 60 percent of the total outstanding amount. On a loan of ₹3 lakh, that could mean paying just ₹1.2 to ₹1.8 lakh — permanently and legally closed with a No Dues Certificate in hand.

When Should You Settle a Personal Loan?

Settling a personal loan is a last resort not a first response to a tough month. It makes sense when the following are true:

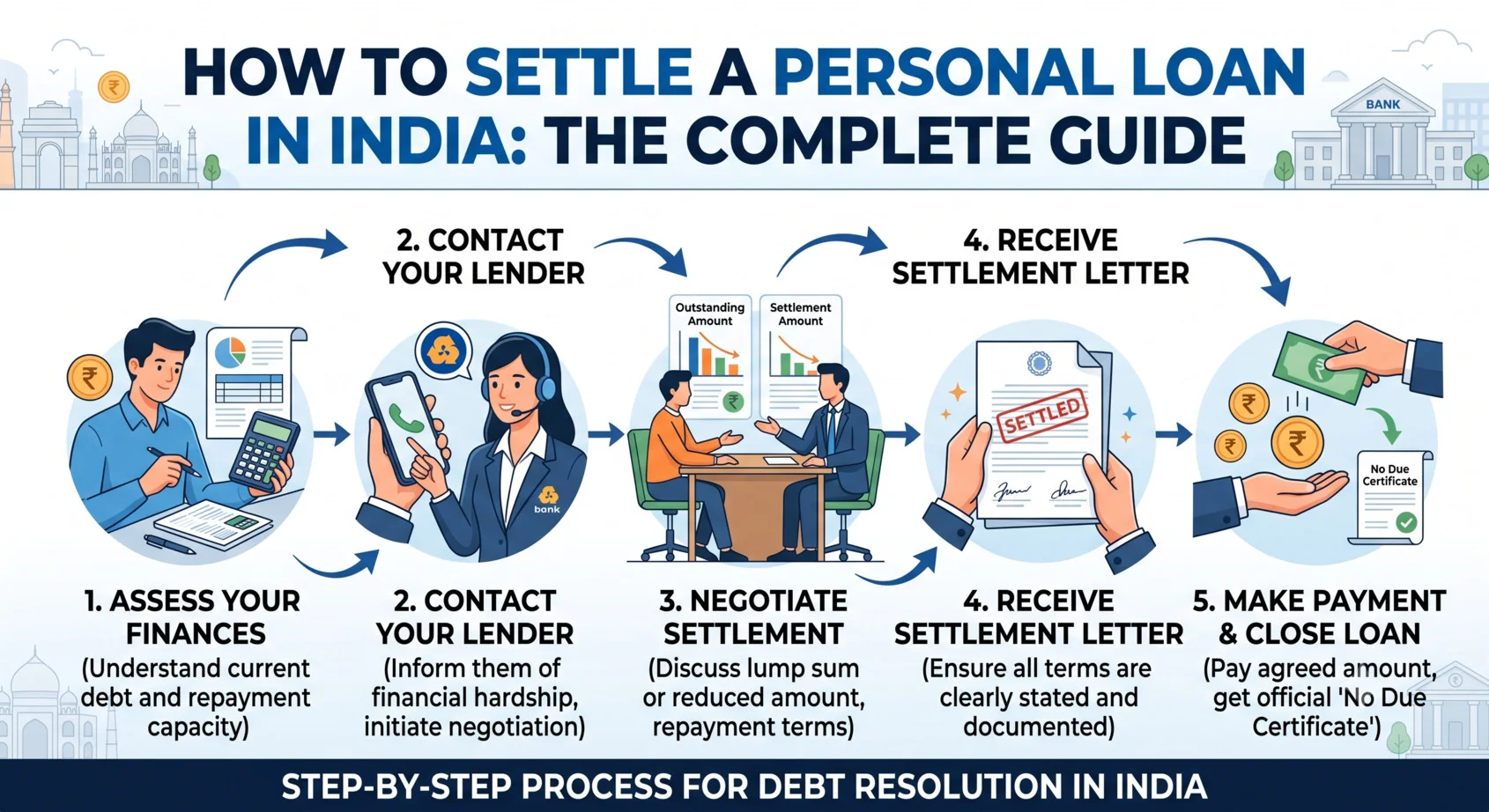

How to Settle a Personal Loan: Step by Step

1 - Know your exact outstanding amount. Request a detailed loan statement showing your principal, accrued interest, and all penalties. This is your negotiating baseline you cannot make a sensible offer without knowing the full number first.

2 - Calculate what you can genuinely pay. Figure out the maximum lump sum you can arrange right now from savings, family support, or selling an asset. Only offer an amount you can actually transfer immediately once the lender agrees.

3 - Approach your lender formally. Write a settlement request letter not just a call. Clearly explain your financial hardship and attach supporting documents: bank statements, salary slips, a termination letter, or medical bills. The more genuine your case looks on paper, the better your outcome.

4 - Negotiate the settlement amount. Your first offer will likely be rejected. That is normal. Go back and forth. A realistic settlement typically lands at 40 to 60 percent of total outstanding. This is where most borrowers struggle without help lenders negotiate every day and most borrowers do not.

5 - Get the settlement letter in writing. Before you pay a single rupee, obtain a Full and Final Settlement letter from your lender. This letter must state the agreed amount, your loan account number, and confirmation that payment closes the loan permanently. This document is your legal protection never skip this step.

6 - Pay and collect your No Dues Certificate.Pay and collect your No Dues Certificate. Transfer the agreed amount through the lender's official channel and keep all receipts. Follow up to collect your No Dues Certificate (NDC) — the document that officially closes your loan account forever.

Why Going Alone Is Risky

Many borrowers try to settle a personal loan by calling their bank directly. While this is possible, it almost always leads to worse outcomes. Banks have trained OTS and recovery teams who do this every day. They know what to say, what to reject, and how to stall. A borrower walking in alone without knowing what to offer, how to present their case, or what documents to submit typically ends up paying more than they needed to, or gives up entirely.

This is exactly why working with a loan settlement expert changes the outcome significantly. An experienced expert knows each lender's OTS thresholds, how to frame a hardship case, and what triggers a faster and lower settlement offer.

How Zavo Helps You Settle a Personal Loan

Zavo is India's most trusted loan settlement platform built specifically to help borrowers settle personal loans, credit card dues, and other unsecured debt directly with lenders, without middlemen, without upfront fees, and without the stress of negotiating alone.

- 97% success rate the highest verified settlement rate of any platform in India

- Over 10 lakh verified users and ₹1,100 crore in debt resolved

- Zero upfront fees you pay only after settlement is confirmed in writing

- No middlemen Zavo negotiates directly with your lender from day one

- Collection calls ease out once the formal process begins

- Cashback on successful settlement

- CIBIL score recovery guidance after settlement

- 1,000+ lenders covered across every major bank and NBFC in Indi

- Rated 4.3 out of 5 by 3 million+ Indian

What Happens to Your CIBIL Score After Settling a Personal Loan?

After you settle a personal loan, your credit report will show the account as "Settled" instead of "Closed." This does have a short-term negative effect on your CIBIL score typically a drop of 75 to 100 points because it signals that the full amount was not repaid.

But here is the perspective most people miss: if you are already missing EMIs and defaulting, your score is already falling every single month. Settlement stops that ongoing damage at a defined point. A "Settled" tag is significantly better than a continued "Default" or "Written Off" status both of which keep pulling your score down indefinitely.

With responsible credit behaviour after settling paying other bills on time, keeping credit utilisation low, avoiding new defaults most borrowers recover their CIBIL score within 2 to 3 years. Many Zavo users qualify for fresh credit within 12 to 18 months of completing their settlement.

Frequently Asked Questions

Q1. Is it legal to settle a personal loan in India?

Yes, completely legal. Settling a personal loan through a One-Time Settlement is fully permitted under RBI guidelines. Banks and NBFCs have formal OTS policies for borrowers in genuine financial hardship. Every settlement is formally documented with a written agreement, payment receipts, and a No Dues Certificate.

Q2. How much will I have to pay to settle my personal loan?

Most Indian borrowers settle personal loans for 40 to 60 percent of the total outstanding amount. The exact figure depends on your lender, the outstanding balance, and how long the account has been in default. Zavo negotiates directly to get you the lowest possible settlement amount across 1,000+ lenders in India.

Q3. Can I settle a personal loan even if I haven't missed EMIs yet?

Technically possible but very rare. Banks typically entertain settlement requests only after an account has been in default for 90 days or more. If you have not yet missed EMIs but foresee trouble ahead, first explore EMI restructuring, a moratorium, or loan relief schemes from your lender before going down the settlement route.

Q4. How long does it take to settle a personal loan?

Most cases resolve within 30 to 90 days from the time you make your first formal settlement request. The timeline depends on your lender's internal OTS process and the number of accounts being settled. With Zavo managing the process, cases typically move faster because of direct lender relationships and experienced negotiators.

Q5. Will my CIBIL score recover after I settle my personal loan?

Yes. After settlement, your account shows as "Settled" on your CIBIL report, which has a short-term negative impact. But with responsible financial habits paying other EMIs on time, keeping credit utilisation low most borrowers recover their CIBIL score within 2 to 3 years. Zavo also provides post-settlement guidance to help you rebuild your credit profile faster.

Ready to settle your personal loan in India? Read the full guide and get started with Zavo — zero upfront fees, 97% success rate, direct lender access.