.webp)

Loan settlement is one of those financial topics that most people only discover when they desperately need it. Here's everything you should know before you're in that position.

The Growing Reality of Loan Default in India

India's retail lending market has grown massively over the last decade. Personal loans, consumer durable loans, credit card debt borrowing has never been more accessible.

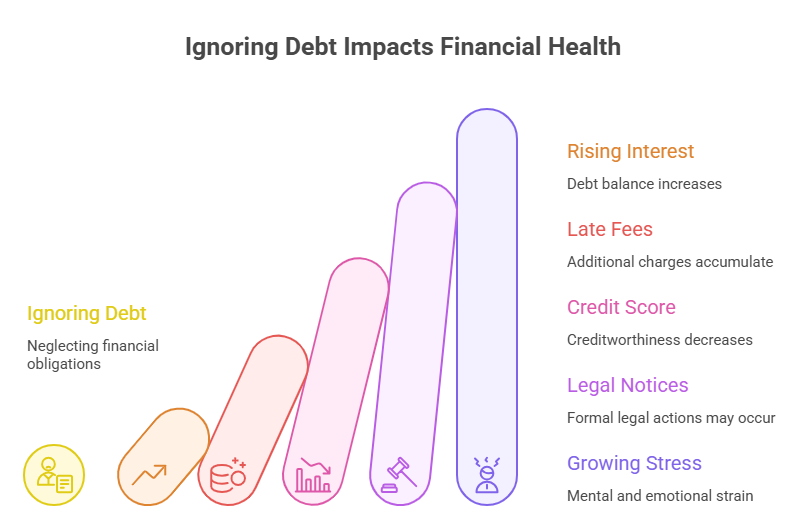

But life doesn't always go according to plan. Job losses, salary cuts, health emergencies, business downturns any of these can turn a manageable EMI into an impossible burden overnight.

When that happens, borrowers are often left with two choices that feel equally bad: keep defaulting and let the damage pile up, or find a legitimate way to close the chapter.

Loan settlement is that legitimate way. And understanding it properly before emotions and pressure cloud your judgment puts you in a far stronger position.

What Is Loan Settlement in India?

Loan settlement is a formal agreement between a borrower and a lender where the lender agrees to accept a reduced lump-sum payment to close a loan account.

The remaining amount the difference between what you owed and what you paid is written off by the lender. The account is then marked as "Settled" in the credit bureau records.

This is different from:

- Loan restructuring - where the terms are changed but you still repay the full amount

- Loan waiver - where the entire outstanding is forgiven (very rare, mostly in agricultural contexts)

- Loan closure - where you repay everything in full

Settlement sits in the middle partial repayment, full account closure.

Is Loan Settlement Legal in India?

Absolutely yes.

Loan settlement is a recognized and practiced financial mechanism in India. The Reserve Bank of India's guidelines on NPA management allow banks and NBFCs to negotiate settlements with defaulting borrowers.

In fact, lenders have dedicated teams often called loan resolution teams or NPA management teams whose specific job is to negotiate and process settlements.

There is no law in India that prohibits a borrower from negotiating a settlement. It is entirely within your rights to approach your lender and request it.

When Do Lenders Agree to Settle?

Lenders don't settle every loan. They settle loans where:

- The account has been in default for 90 days or more (NPA classification)

- The borrower can demonstrate genuine financial hardship

- Recovery of the full amount through legal means is unlikely or costly

- A lump-sum settlement offer is on the table

The key is that lenders are businesses. They make rational decisions. If they calculate that settling for 50% today is better than spending two years in legal proceedings to maybe recover 60%, they'll settle.

Understanding this logic helps you negotiate from a position of knowledge rather than desperation.

How Loan Settlement Affects Your CIBIL Score The Full Picture

This section deserves careful reading because there's a lot of misinformation floating around.

What actually happens: When your loan is settled, CIBIL and other credit bureaus update your account status from whatever it was (likely "Sub-standard" or "Doubtful" due to default) to "Settled."

The impact: "Settled" is not as good as "Closed" from a credit score perspective. Future lenders can see that the full amount was not repaid. This can affect loan approvals, especially in the short term after settlement.

The context most people ignore: If your loan was already in default for 90+ days, your score was already significantly damaged. At that point, settlement:

- Stops the ongoing negative reporting

- Closes the account definitively

- Gives you a clean starting point to rebuild

The "Settled" status remains on your report for 7 years. However, credit scores are dynamic. With consistent positive behaviour post-settlement, many borrowers see meaningful score recovery within 12–24 months.

Bottom line: Settlement hurts your score less than continued default does. And it gives you something continued default never will a closed account and a defined starting point.

Types of Loans That Can Be Settled in India

Most unsecured and some secured loans can be settled:

Commonly settled:

- Personal loans

- Credit card outstanding dues

- Business loans (unsecured)

- Consumer durable loans

- Education loans (in some cases)

Harder to settle but possible:

- Home loans

- Loans against property

- Vehicle loans

For secured loans, lenders have the option to repossess collateral which gives them less incentive to settle. However, settlement is still possible if the collateral value doesn't cover the outstanding or if legal proceedings are costly.

The Step-by-Step Process of Loan Settlement in India

Step 1 - Evaluate your financial position Determine what lump sum you can realistically arrange. This is your settlement budget.

Step 2 - Pull your credit report Know how your loan is currently classified. NPA accounts have more settlement room.

Step 3 - Contact the right team Don't call general customer care. Ask specifically for the loan resolution, NPA, or collections settlement team.

Step 4 - State your case clearly Explain your financial hardship. If you have documentation job termination letter, medical bills, bank statements showing income drop use them. They strengthen your case.

Step 5 - Negotiate The lender's first offer is rarely their best. Negotiate. Know your floor (what you can actually pay) and don't go above it.

Step 6 - Get written confirmation A settlement letter on the lender's letterhead, stating the agreed amount and terms, before any payment is made.

Step 7 - Pay and collect NOC Pay via traceable mode NEFT, RTGS, or cheque. Collect your No Objection Certificate after payment.

Step 8 - Verify credit report update Check your credit report 45 days after settlement to confirm the status has been updated correctly.

Why Many Borrowers Use Settlement Platforms

Negotiating directly with a lender is possible but it has real challenges:

- You may not know what settlement percentage is reasonable for your loan type

- Lenders' internal teams are experienced negotiators - you're not

- Without the right language and documentation, you may accept a higher amount than necessary

- The process can drag on for weeks without a clear outcome

This is why dedicated loan settlement platforms have grown significantly in India. Platforms like Zavo work directly with lenders cutting out middlemen, speeding up the process, and typically securing better settlement terms than individuals can negotiate alone.

What makes Zavo particularly notable:

- Direct lender access - No third-party intermediaries

- 97% success rate - Across 10 lakh+ verified users

- Cashback on successful settlement - An actual financial benefit on top of the settlement

- Post-settlement credit rebuilding - Structured tools to recover your CIBIL score after settlement

For anyone dealing with multiple overdue loans or who has already tried negotiating without success, a platform like Zavo can make the difference between a good settlement and a great one.

What to Do Immediately After Loan Settlement

Settlement is the end of one chapter and the beginning of another. Here's how to start the next one right:

1. File your NOC safely This document is your proof. Store it digitally and physically.

2. Monitor your credit report Ensure the "Settled" status is updated correctly. Dispute any errors immediately.

3. Start rebuilding credit immediately Don't wait. Get a secured credit card, make small purchases, pay in full every month.

4. Avoid new debt for 6–12 months Give your financial situation time to stabilize before taking on new obligations.

5. Use a credit builder program Structured programs help you systematically improve your score with real credit-positive activities.

Common Mistakes to Avoid During Loan Settlement

Paying before getting written confirmation - Always settlement letter first, payment second.

Accepting the first offer - Always negotiate. The first number is rarely the best number.

Not verifying the credit report update - Follow up until you see the correct status.

Settling without being able to pay the agreed amount - If you commit and can't pay, you've weakened your negotiating position significantly.

Ignoring post-settlement credit repair - The settlement is only half the battle. Rebuilding is the other half.

Final Thoughts

Loan settlement in India is a legitimate, practical, and widely used financial tool. It's not a loophole or a shortcut it's a structured process that exists precisely because life doesn't always go according to plan.

If you're dealing with overdue loans, the worst thing you can do is ignore the situation. The best thing you can do is understand your options clearly and act on them before the window for reasonable settlement closes.

Whether you negotiate directly or use a platform like Zavo the goal is the same close the debt, stop the damage, and start rebuilding.

That fresh start is closer than it feels right now.