Applying for a new loan requires you to prepare your credit report. Determine the basic details, employment details, pending debts, and delinquencies (if any). Every aspect, like name, residential address, income, payments, and citizenship, should be true to your knowledge. A responsible loan company checks and verifies your personal and financial aspects before approving a loan.

Moreover, if your profile reveals a good series of heavy debts, your approval may be affected. Therefore, clearing some dues before applying may help. It reduces the credit utilisation ratio, improves your credit score, and makes you eligible for better interest rates. The blog discusses how you can approach repaying pending debts before applying for a loan.

7 Steps to pay dues before getting another loan

If you are keen on improving the prospects of getting the best personal loans for bad credit scores, the following ways to repay dues may help.

Step 1- identify how much you need

Yes, the type of loan and the amount matter when you want to repay the pending debts. For example, if applying for a mortgage or home renovation loan, you must not have any bankruptcy or pending secured debt in your credit history.

It may affect the loan approval, as your credit profile does not have much scope for a new and heavy loan. Thus, you must clear the secured loan first to get a loan. Similarly, if you need over £50000, then you will have to consolidate or pay higher-interest debts first.

Step 2- Understand the new loan criteria

Unless you know the eligibility criteria for the new loan, you may be flying in the dark. Identify the basic loan eligibility criteria by pre-qualifying. Moreover, you can check the respective website or use an eligibility checker to determine your loan approval chances.

Analyse where you lack and what you can do to improve it. For example, if applying for a home loan, you need 3 years of constant residential history as a UK citizen. Therefore, you must ensure citizenship until that term. Similarly, you need a basic affordability test using a debt-to-income ratio based on living expenses, debt repayments, and utility bills.

Step 3- identify how much you owe

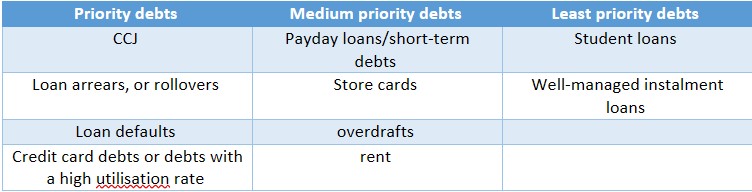

First, calculate the total amount that you owe on different dues. Include the added interest, penalties, late payment charges, etc. Do so with every due that you want to clear now. Now, check how much you need to pay in total. You can check the dues on debts like rent, utility payments, payday loans, overdrafts, renovation loans, car repair pending dues, etc.

- Step 4- How much can you repay

Determine how much you can pay depending on your current financial status. Finances do not remain the same from the first day you took the loan. Therefore, analyse the recent changes in your income, monthly expenses, and new goals.

Check how much you can dedicate to paying the dues before applying for a new loan, such as a mortgage. Having a clear idea of how much you can pay helps you decide the amount you can get or borrow on the next loan.

Step 5- Try to negotiate with creditors

It is one of the most important aspects to consider while repaying the year-long dues. Check whether you can negotiate the payments with creditors. It is especially important if you have been struggling to pay one for some time.

The creditors may agree to negotiate if you pay part-payments at least on the loan. Doing so with every creditor may help you save money on interest and the total cost repayable. Therefore, it reduces your liabilities and makes it easier for you to clear the dues.

Step 6- Avoid applying for new loans (before 30 days)

You must be planning to take a big loan, such as a home renovation, a mortgage, or an instalment loan, to achieve major lifestyle goals.

However, one is habitual to taking small loans to fix emergencies or unnecessary expenses like buying a dress or any other instinct-based purchases. It may affect your budget and ability to pay off a big loan. Moreover, it also impacts the chances of getting a loan. You should instead keep a safe emergency fund ready to handle such aspects.

Step 7- Seek free debt advice

You can also check out the best ways to clear your dues according to your personal finances, income, and spending habits. Taking help from industry experts may help you fetch a suitable solution for your finances. You can then be loan-ready by repaying the previous dues according to what you can afford.

What mistakes should you avoid while paying off debts?

Now, let’s understand the mistakes that you should avoid while clearing the dues:

Avoid closing old accounts

Most individuals make mistakes by closing the old bank accounts that they hardly use. It affects the credit history that you build up over the years. Therefore, don’t close any old account. It is regardless of how little you use it.

Avoid taking high-cost credit

If you are taking a costly loan just to boost your credit rating before seeking a new loan, then it may prove to be the greatest mistake. What if you fall on finances? What if it does not help you achieve the desired goal? If you end up missing a payment, the new loan will become more of a liability and may affect your credit score further.

Don’t ignore small arrears

If you generally skip the small loan arrears, then you could be making a costly mistake. Loan providers check out for every arrear before providing important loans like home renovation loans, mortgages, personal loans, or payday loans. Therefore, always try to clear all the arrears before applying for a new loan. Otherwise, it may affect your loan application approval.

Bottom line

Thus, these are some ways to settle debts before applying for a loan in the UK. Identify what the new loan expects of you and the eligibility criteria. Accordingly, identify what you need to work on to get a quick loan at better interest rates. Check the dues, which may help you improve the credit utilisation ratio drastically. Try to pay them first.